Blockchain technology can be a game-changer by helping to collect and track data. It can be used to address a wide range of issues in supply chain management and Logistics Management. In addition to recording or tracking, there are several other ways blockchain technologies can help supply chains function.

This cooperation aims to disrupt the supply chain financial system by tracking the flow of goods and services and the supply chain itself. This allows for product traceability throughout the process, which in turn leads to a more efficient and transparent supply system.

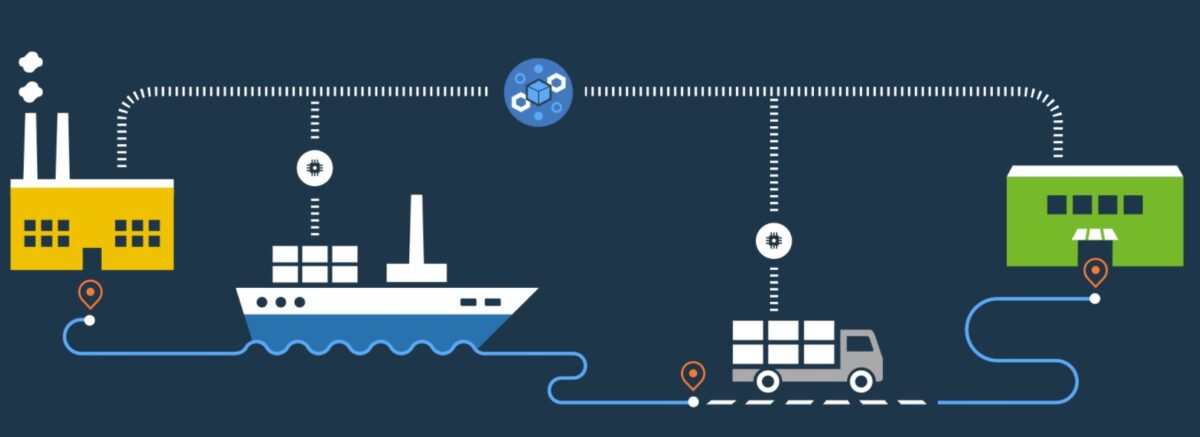

Blockchain-based Supply Chain Management enables provenance tracking, which allows information to be collected about the origin, production, and delivery of a product from a single source, such as an embedded sensor. If a company detects a defective product, blockchain enables the company and its supply chain partners to track the product and identify all suppliers involved, identify the associated production or supply quantity, and recall it efficiently.

Companies across all industries are exploring blockchain applications, motivated by regulations requiring them to prove the origin of their products and by downstream customers seeking the ability to trace components of inventory. These applications are supported by well-defined use cases, and companies are exploring the potential of blockchain as a means of traceability in the production and distribution of goods and services.

Blockchain is a decentralized register of information on the origin, production, and distribution of goods and services. The inspection and tracking of products along the entire supply chain give retailers the information they need to communicate like the origin of products to consumers, build trust, and gain a share of the purse. It minimizes duplication and expense problems, provides proof of ownership for digital coins, and provides a one-stop-shop for all suppliersand customers of a product or service. Blockchain is an open, distributed and decentralized register for the production, distribution, and ownership of product and service information.

Blockchain is valuable because it includes blocks that integrate all three types of transaction flows and capture details that are not recorded in financial accounting systems. Blockchain is a distributed ledger technology that allows for a fixed record of transactions without intermediaries such as banks. It is ideal to track the origin of goods because a common digital register creates fixed records of all transactions. As the distributed register is decentralized, all parties will receive a copy that prevents a single failure point or data loss.

What is now clear is that a supply chain based on a single blockchain is unlikely. To take advantage of blockchain in the supply chain industry, companies should start integrating new systems today. Once industry-wide standards are in place, they can build on these standards to create a common, unauthorized blockchain environment.

It is important to note that blockchain would not replace all transactions, accounting and management functions performed by the ERP system and its corresponding inventories and transactions. By linking inventory information and financial flows and sharing them with all parties to a transaction, blockchain enables companies to match orders, invoices, and payments and track the progress of transactions between counterparties. It is difficult to assess the flow of diary entries, receivables, or credit repayments, even if these types of outflows are recorded by ERP systems. Another activity that can be improved in the management of complex processes, including the adaptation of invoices to orders and the monitoring of payment terms, as well as the implementation of controls and releases at every step.

The process that connects all parties involved in the delivery of the finished product is called the supply chain. Supply chains operate in different ways, have different characteristics, but they all operate in the same way.

From cryptocurrencies to digital voting to cloud storage, technology affects almost every industry, and retail is no exception. In addition to the potential for upheaval in the financial world, there is also a potential for upheaval in other sectors such as health care, education, finance, and healthcare.

To achieve this, the Bitcoin network consumes a large amount of energy to promote Bitcoins and is vulnerable to hackers. Because data is invariable and decentralized, blockchain technology is a key element of this innovation wave, which should be key to any innovation wave.

Retailers are expected to spend more than $15 billion on digital advertising this year, and the advertising industry is plagued by fraud, privacy breaches, and data theft.

This ensures that transactions on the network are accepted by the majority of subscribers, but unfortunately it also limits the speed at which new blocks can be added. Besides, each blockchain subscriber receives a unique identifier or digital signature to sign the blocks they add to the blockchain. More specifically, because blockchains are inherently invariable, data on a blockchain cannot be modified after it has been added to it. Also, no participant can overwrite past data, as this would mean that subsequent blocks would have to be rewritten in a shared copy of the blockchain.

At the most basic level, blockchain’s core logic means that no stock can exist twice in one place. This last-minute stress is necessary because the blockchain network records every possible disturbance to ensure better and exceptional treatment.

For example, a company could borrow money from several banks for the same asset, apply for a loan for one purpose, and then use it for another. X, an action can take place if a certain number of conditions are met. This is because blockchain is used to control credit and underpin smart contracts. Smart contracts are powered by blockchain, but they are also a key element of the supply chain system.

Smart contracts can be programmed to evaluate the status of a transaction and automatically initiate actions such as the release of payment, registration of an entry, or marking of an exception that requires manual intervention. Blockchain smart contracts can also be modified to include programmable clauses that allow invoices to be issued and processed once a set of conditions are met.